HIGHLIGHTS OF THE WEEK

- U.S. economic data disappointed on a variety of fronts this week, but much can be chalked up to weather-related disruptions to the data.

- A paltry 89k payrolls gain was the biggest disappointment, but we are inclined to look past one month’s result and focus on a new cyclical low in unemployment and continued improvement in measures of underemployment. These should also help support a rebound in consumer spending through the remainder of 2017.

- In other news, the Fed is starting to discuss the process of unwinding its holdings of Treasuries and mortgage-backed securities (MBS). It pledged that moves will be well-telegraphed and are likely to start later this year.

[su_row][su_column size=”1/2″]

[/su_column]

[su_column size=”1/2″]

[/su_column][/su_row]

BLAME IT ON THE WEATHER

March payrolls data disappointed expectations, with only 98k new jobs in March, and downward revisions to hiring in January and February. A softer reading was expected after two heady months, but a 200+ reading in the closely watched ADP report earlier in the week had raised hopes. Hiring slowed across both the goods and services sectors, although it was more dramatic in services. Despite the unexpectedly weak payroll print, the household survey showed employment gain of 472k, pushing the unemployment rate down by 0.2 percentage points to 4.5%.

We are inclined to look past one month’s payrolls disappointment. Weather played a role in the March data on two fronts. Unusually warm weather in January and February  likely pulled forward activity in the construction sector. And, data on curtailment of hours due to bad weather was nearly ten times larger than average in March, impacting hours worked, earnings and potentially hiring.

likely pulled forward activity in the construction sector. And, data on curtailment of hours due to bad weather was nearly ten times larger than average in March, impacting hours worked, earnings and potentially hiring.

The job market should continue to provide a solid foundation for consumer spending this year, with the unemployment rate near pre-recession lows in March, and continued improvement in measures of underemployment.

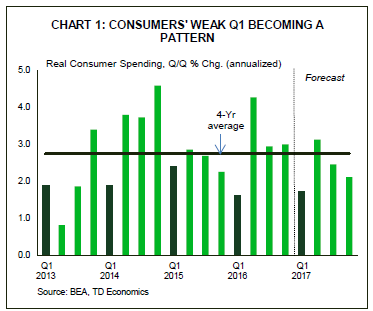

Other data this week confirmed that consumers took a breather once again in Q1, but we expect a rebound in spending in Q2, much like we saw last year. Q1 weakness has become a pattern. Consumer spending growth averaged 2% in Q1 over the past 4 years, while the other three quarters of the year have averaged above 3% (see chart). Eventually, this pattern will be fixed by adjustment to “seasonal adjustment,” but for now we are inclined to discount Q1 weakness.

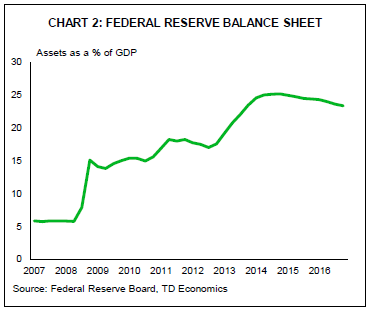

The Fed minutes also provided a peek into the FOMC’s discussion of how and when it will start the process of normalizing its balance sheet, now that normalizing rates is underway. Through the course of its asset purchase program, the Fed accumulated $4.5 trillion in Treasuries and MBS. Since purchases ended, the Fed has been reinvesting the principal payments, keeping its balance sheet steady.

Although things are still at the discussion phase, Fed members already agree on a few things. First, the process of ending reinvestments should be gradual and predictable, and rely primarily on passive phasing out of reinvestments. Second, most members agreed that the change in reinvestment policy should come this year. Third, the FOMC was unanimous that any policy change should be well telegraphed to the public. Our recent forecast calls for the Fed to  hike rates in two 25 basis point moves, likely in June and September, and then lay out the plan to start winding down reinvestments. Once reinvesting principal payments is completely phased out, the balance sheet will passively shrink as the securities mature.

hike rates in two 25 basis point moves, likely in June and September, and then lay out the plan to start winding down reinvestments. Once reinvesting principal payments is completely phased out, the balance sheet will passively shrink as the securities mature.

Markets are watching closely since removing the Fed from these markets could reduce demand for these securities, lowering prices, and taking yields higher, all else equal. Our latest forecast calls for a continued rise in Treasury yields, and balance sheet normalization is one of the forces expected to take yields higher. The Fed has control of this process. If the Fed doesn’t like the market reaction as it winds down reinvestments, it has the discretion to slow down or stop the pace of adjustment. This helps to mitigate the risks of an undesirable spike in yields.

Leslie Preston, Senior Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.