FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Despite delivering a widely anticipated quarter-point rate hike this week, the Fed’s more hawkish outlook for the pace of future rate hikes saw Treasury yields jolt higher.

- In our updated forecast we refrain from jumping on the fiscal stimulus bandwagon, given that significant policy shifts remain speculative at this point.

- In the meantime, higher bond yields will filter through to higher borrowing rates for consumers and businesses, and will ultimately diminish the need for Fed hikes. As such, our expectation for a very modest

pace of Fed hikes remained unchanged in our forecast.

[su_row][su_column size=”1/2″]

[/su_column]

[su_column size=”1/2″]

[/su_column][/su_row]

WHAT FISCAL POLICY GIVES, MONETARY POLICY MAKE TAKE AWAY

Despite delivering a universally expected quarter-point rate hike this week, the Fed still managed to jolt markets. Its slightly more hawkish rate outlook, with the median ‘dot’ now indicating one additional rate hike during 2017 for a total of three, took markets by surprise with the U.S. 10-Year bond yield surging 15 basis points since. Yellen characterized the shift as “modest”, and indicated it reflected some of the participants incorporating fiscal stimulus into their projections. She also made clear that with the economy very close to full employment, what fiscal policy gives in stimulus, monetary policy is likely to take away with faster rate hikes.

Clearly some FOMC members agree with markets’ assessment that fiscal policy is about to get more stimulative under a Trump administration. In our new Quarterly Economic Forecast, we refrained from jumping on the ‘optimism bandwagon’ that has been driving markets since the election. While we believe that many aspects of Trump’s platform could raise inflationary pressures – including restricted immigration and higher import tariffs – a significant fiscal stimulus package is far from a done deal.

We acknowledge that the Republican sweep in Washington is likely to yield significant policy changes, in particular on tax reform, deregulation and the Affordable Care Act. But, it is not at all certain how large a stimulus is in the offing. Many Congressional Republicans are determined to rein in the deficit, which already sits at approximately 3% of GDP, and will require new taxes or spending cuts to balance. On the campaign trail, Trump indicated that he would find savings to offset his tax cuts. He proposed to cut non-defense discretionary spending by 1% every year – the so-called “penny plan”. After ten years this would amount to a 25% spending cut in absolute terms versus current projected levels, and would produce a notable economic drag.

Reforms on the corporate side, including regulatory changes and tax cuts, could help to improve the climate for business investment, which hasn’t contributed much to growth over the 2015-16 period (Chart 1). But we would need to get more clarity on government policy initiatives before we adopt formal changes to our forecast.

In the meantime, higher Treasury yields will surely trickle through to borrowing rates for consumers and businesses. Combined with the sizeable appreciation of the U.S. dollar, this represents a tightening in financial conditions. This will likely weigh on the pace of investment in housing over the next couple of years , and a stronger currency is likely to lead to larger economic drag from trade.

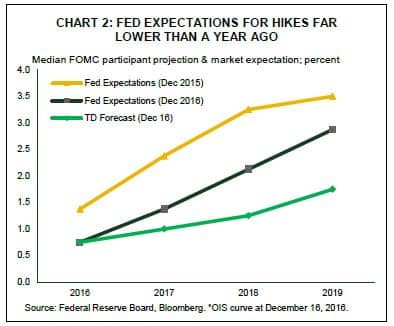

Those impacts illustrate how, to a large extent, bond markets are doing the Fed’s tightening work for it. Higher rates farther out the curve lower the need for tighter policy going forward, rather than increase it. We suspect that this dynamic will contain the Fed to one hike in each of 2017 and 2018 – below others’ expectations (Chart 2). It is also worth noting that at this time last year the Fed thought it would be raising rates four times, not once, in 2016. All told, the high degree of uncertainty about fiscal policy and the reality that its impact on the economy is likely to be quite lagged suggests there is, once again, plenty of room for disappointment as far as future pace of Fed hikes is concerned.

Leslie Preston, Senior Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.