FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Domestic data took a backseat to this week’s developments out of Europe with major political developments in Italy early in the week.

- On Thursday, the ECB revealed a reduction to its monthly asset purchases beginning in April of next year. The move was applauded by markets and seen as a dovish taper with ECB President Mario Draghi making it clear that this was a one-time adjustment and not a tapering down to zero.

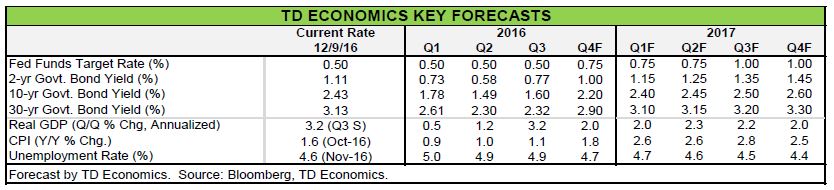

- Data out of the U.S. did less to move markets, but continued to paint a picture of a solid domestic economy. With the much anticipated December FOMC meeting just around the corner, we are almost certain that the Fed will continue along its “gradual” hiking path come next Wednesday.

[su_row][su_column size=”1/2″]

[/su_column]

[su_column size=”1/2″]

[/su_column][/su_row]

INTERNATIONAL DEVELOPMENTS TAKE CENTER STAGE

The domestic data calendar took a backseat to this week’s developments out of Europe. To kick things off, markets were taking the ‘no’ outcome of Sunday’s Italian referendum quite constructively. This was despite the political risk attached to PM Renzi’s forthcoming resignation and the perception of a ‘no’ vote as supportive of Beppe Grillo’s Five Star Movement party. With a vast majority of Italians in support of remaining in the EU and retaining the euro, the fear that a ‘no’ vote would eventually lead to a UK-style exit from the EU was likely overstated.

Political news out of Austria provided markets with something else to cheer about. Presidential elections declared pro-EU candidate, Alexander Van der Bellen, as the winner, putting fears to rest that another forthcoming referendum on the EU, as campaigned upon by the far right Freedom Party, was on its way. To top these developments off, an unexpected resignation by New Zealand’s Prime Minister, John Key, added to the political uncertainty that had already materialized over the weekend in Italy.

The main event came later on in the week as the ECB’s policy decision came to light. At the conclusion of the meeting, the ECB’s Governing Council agreed to leave interest rates unchanged. However, the pace of asset purchases were adjusted such that they would fall by €20 billion to €60 billion per month in April 2017 and remain at that level through the end of December or beyond if deemed necessary. The decision to leave monetary conditions at a currently highly accommodative stance through 2017 bodes well for the gradual economic recovery in the Euro area and was

applauded by global market participants.

Things were less interesting at home. Second and third tier economic data did little in the way of moving markets. Of note was the rebound in the ISM’s gauge of the services sector in November, which rose to a 13-month high (Chart 1). Particularly encouraging were the gains seen in the business activity and employment sub-indices. Taken together, both components suggest that economic activity has accelerated after a slow start to the fourth quarter that may have been related to pre-election uncertainty and impacts of Hurricane  Matthew.

Matthew.

Countering some of this optimism was trade data for October, which revealed a broadly anticipated widening of theinternational trade deficit, a development that underscores the relatively weak external environment further exacerbated by a strong U.S. dollar and rising political uncertainty (Chart 2). Both U.S. dollar strength and political uncertainty will remain a dominant theme in 2017, likely acting as a drag on U.S. GDP over the next year.

Nonetheless, this week’s developments are unlikely to figure into next week’s much anticipated interest rate decision by the FOMC. Markets have been pricing in a 100% probability of a hike for over a month now, providing the FOMC with a strong signal that it is time to move along the Fed’s “gradual” hiking path. Domestic data has also been largely supportive, with the average pace of jobs growth coming in well above trend and firming wage growth continuing to nudge inflation towards the Fed’s 2% target. As such, we are almost certain that the fed funds range will be 25 basis points higher come Wednesday next week.

Neil Shankar, Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.