HIGHLIGHTS OF THE WEEK

- Markets sold off sharply this week, following a somewhat hawkish assessment of the U.S. economy from the Fed’s new chair Jerome Powell and the announcement of steep tariffs on steel and alumimium imports by Donald Trump.

- Despite the market reaction to Powell’s comments, there was not much in the data this week to indicate that the economy is overheating. Both headline and core PCE inflation remained unchanged in January, coming in at 1.7% y/y and 1.5% y/y, respectively. Real consumer spending fell by 0.1% on the month. Vehicle sales also weakened in February.

- Both consumption and GDP will start the year on a softer footing but weakness is expected to be short-lived. Tax cuts and tightening labor market will support consumer spending and above-trend growth over the remainder of 2018.

Fears of Trade War Rattle Financial Markets

This was a busy and difficult week for financial markets. Economic data releases were overshadowed by the much anticipated first Congressional testimony by the new Federal Reserve chair Jerome Powell and trade tariff announcement from the White House.

This was a busy and difficult week for financial markets. Economic data releases were overshadowed by the much anticipated first Congressional testimony by the new Federal Reserve chair Jerome Powell and trade tariff announcement from the White House.

In his speech on Tuesday, Mr. Powell struck an upbeat tone on the U.S. economy and inflation, saying that his “outlook for the economy has strengthened since December.” He also highlighted potential upside risks to growth and inflation stemming from fiscal policy and the improved global economic backdrop. Without stating the exact number of rate hikes expected this year, Powell seems to have opened the door to a faster rate of normalization as long as the economic data cooperates. Markets were quick to interpret his comments as hawkish, with equities selling off and bond yields rising. New York Federal Reserve president Bill Dudley added more fuel to the fire by saying that four rate hikes by the Federal Reserve this year would still constitute a “gradual” pace of tightening.

Market losses extended further on Thursday on fears of trade wars following Donald Trump’s announcement of a 25% import tariff on steel and 10% on aluminum. While nothing has been signed yet, should these tariffs be introduced, they will lead to higher input prices for many manufacturing and construction industries which rely heavily on steel and aluminum inputs and ultimately result in higher prices for U.S. consumers, thus posing an upside risk to the Fed’s inflation outlook. The Fed may look through a one-time change in prices as a result of tariffs, but will be cautious on the impact on inflation expectations and potential economic growth – trade wars are not typically good for productivity growth.

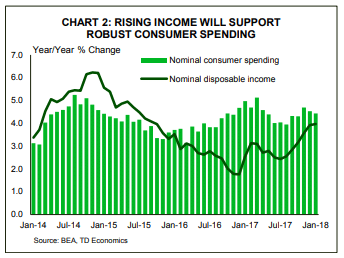

Still, for the time being there is not much in the incoming data to indicate that the economy is overheating. Inflation-wise, both headline and core PCE inflation remained unchanged in January, coming in at 1.7% y/y and 1.5% y/y, respectively. Real consumer spending fell by 0.1% on the month, despite strong gains in real disposable income (+0.6% m/m) on the back of lower taxes. Indicators of housing activity were also soft. Coming on the heels of a decline in existing homes, January sales of new homes and the forward looking pending sales of existing homes also weakened. Ditto for auto sales, which edged down to 17.0 million units in February from 17.1 million in January. All in all, similar to the prior years, both consumption and GDP will start the year on a softer footing.

That being said, the slowdown will likely be short-lived. Some of the weakness in consumption is likely a pullback from the hurricane-induced ramp up at the end of 2017, and some due to “residual seasonality,” which has become apparent in recent years. Barring unexpected developments trade-side, tax cuts and a tightening labor market will prop up household income this year, supporting robust consumer spending and above-trend growth over the remainder of 2018.

All in all, the latest data does not change the calculus for the Fed with three rate hikes expected this year, however, the central bank will certainly need to keep a close watch of the economy, given rapidly evolving U.S. public policy.

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.