HIGHLIGHTS OF THE WEEK

- Domestic equity markets shrugged off news that the U.S. administration is pulling out of the current Iran deal while leaving the door open to renegotiation.

- WTI oil rose for a fifth consecutive week. Rising U.S. gasoline prices helped drive headline inflation to 2.5% y/y, the fastest pace of price growth since February 2017.

- A loss of momentum in underlying inflation in April should help reduce concerns that the Federal Reserve isn’t moving fast enough to cool a hot U.S. economy.

Upping the Stakes

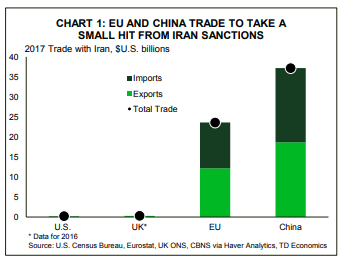

Events this week remind us of how uncertain the world can be at times, and how unpredictable financial markets can be. On Tuesday President Trump announced that his administration will no longer be part of the current Joint Comprehensive Plan of Action (JCPOA). That was a 2015 deal agreed to by the U.S., UK, EU, Germany, France, Russia, and China that lifted sanctions against Iran in return for a promise to pause its nuclear program. Although pulling out of the agreement will have limited direct economic implications for the U.S., the imposition of sanctions on Iran and the threat to do so on those nations that continue to do business with it, is likely to deal a blow to its trade partners (Chart 1).

Events this week remind us of how uncertain the world can be at times, and how unpredictable financial markets can be. On Tuesday President Trump announced that his administration will no longer be part of the current Joint Comprehensive Plan of Action (JCPOA). That was a 2015 deal agreed to by the U.S., UK, EU, Germany, France, Russia, and China that lifted sanctions against Iran in return for a promise to pause its nuclear program. Although pulling out of the agreement will have limited direct economic implications for the U.S., the imposition of sanctions on Iran and the threat to do so on those nations that continue to do business with it, is likely to deal a blow to its trade partners (Chart 1).

Financial markets were caught somewhat off-guard by the decision, with conflicting news headlines generating gyrations throughout the day. Since a renegotiation of the deal is a possibility, markets shrugged off the news, with domestic equity markets likely to end the week up 2%. WTI oil prices also moved higher this week, holding above US$70 on this and other news of escalating Middle East tensions.

Oil prices have been rising steadily over the past five weeks, with implications for the domestic and global economy. Higher energy prices should help support domestic investment and overall economic activity in oil exporting countries such as Saudi Arabia, Canada, and increasingly the United States. However, consumers will likely feel the pinch from higher energy prices, as the rising price of gas reduces their overall purchasing power.The pass-through to consumers from rising energy prices is usually quite brisk, and this time is no exception (Chart 2). The U.S. CPI report for April saw prices rise 2.5% over the past twelve months, largely owing to a strong upward move in the price of gasoline (+13.4% y/y). Aside from energy, shelter costs continue to tick up, a reflection of tight housing inventories in many U.S. cities that is sending home prices higher.

Oil prices have been rising steadily over the past five weeks, with implications for the domestic and global economy. Higher energy prices should help support domestic investment and overall economic activity in oil exporting countries such as Saudi Arabia, Canada, and increasingly the United States. However, consumers will likely feel the pinch from higher energy prices, as the rising price of gas reduces their overall purchasing power.The pass-through to consumers from rising energy prices is usually quite brisk, and this time is no exception (Chart 2). The U.S. CPI report for April saw prices rise 2.5% over the past twelve months, largely owing to a strong upward move in the price of gasoline (+13.4% y/y). Aside from energy, shelter costs continue to tick up, a reflection of tight housing inventories in many U.S. cities that is sending home prices higher.

Abstracting from energy and other volatile prices, underlying price pressures remain fairly subdued despite strong economic activity and tightening labor markets. Core inflation lost some momentum in April, as price growth in core services slowed a touch. Still, core inflation registered a 2.1% gain year-on-year, but that includes a fading base-year effect from the dip in telecommunications prices last year that is acting to prop up inflation.

The loss of inflation momentum may help reduce concerns that the Fed isn’t moving fast enough to cool off a hot economy. Inflation is likely to hold near the Fed’s 2% target for the remainder of the year, with the economy running just hot enough to warrant two more rate hikes this year. That said, downside risks to the domestic and global outlook continue to materialize. Although they have had limited impact thus far, things can quickly escalate. While the Iran sanctions act to elevate the risk of a trade war between the U.S. and its trade partners, all parties appear open to dialogue. Still, this decision adds further pressure on Europe and China to settle trade imbalances with the United States.

Fotios Raptis, Senior Economist | 416-982-2556

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.