FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Investors this week were kept busy with the release of the GOP tax reform plan, which sent small cap stocks higher and the S&P 500 lower immediately after its announcement. President Trump nominated current Federal Reserve Board Governor Jerome Powell to succeed Janet Yellen as Chair of the Fed in February 2018.

- Volatility as a result of Hurricanes Harvey and Irma skewed data released this week, but the outlook for the fourth quarter remains positive, with hiring in October recovering from hurricane setbacks. Inflation continues to disappoint, with core PCE holding steady in September at 1.3% y/y, and wage growth disappointing in October, rising only 2.4% y/y.

- We expect inflation to reach its 2.0% target late in 2018, with robust economic activity in the meantime giving the Fed enough ammunition to proceed with a rate hike this December.

Investors React to GOP Tax Reform Plan

Thursday’s release of the Republican tax overhaul plan finally gave investors more detail to chew on in determining the winners and losers of the most significant reworking of the tax code in over three decades. The plan slashes the top corporate tax rate from 35 to 20%, and the announcement boosted small cap stocks on account of their higher effective corporate tax rate, while the S&P 500 stumbled in the aftermath of the announcement. The proposal to cut the mortgage interest deductibility in half to $500,000 drove a sell-off in homebuilding stocks. This effective tax increase could dent housing demand particularly in high-priced markets, such as Washington, D.C. and Boston where the median home price already exceeds $500,000. Next, the bill will head to the House Ways and Means Committee before going to the House and Senate for approval. Should the plan progress smoothly, investors should look for small caps to appreciate further while large cap stocks will likely struggle as a result of the scaling back of interest payment deductibles. The USD depreciated as investors weighed the

Other events on Capitol Hill this week included President Trump’s nomination of current Federal Reserve Governor Jerome Powell to succeed Janet Yellen as Chair of the Federal Reserve on February 3rd, 2018. Given Powell’s views that align with the FOMC consensus, markets remained calm following the announcement. Moreover, in addition to tax reform prospects, investor sentiment was supported by indications that economic growth is likely to remain strong this quarter.

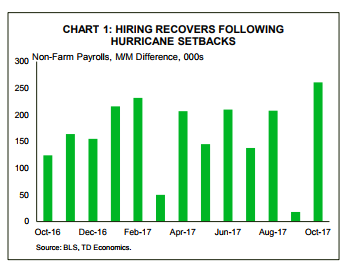

Volatility as a result of Hurricanes Harvey and Irma skewed data released this week, but the outlook for the fourth quarter remains positive and is helped by a solid finish to the third quarter. Strength in consumer spending in September, notably on durable goods, sets the stage for another strong showing from households in the fourthquarter. This was echoed in October’s vehicle sales which remained elevated as consumers replaced flooded cars, something that is expected to gradually fade in the months ahead. A tighter labor market should act to support household spending further. Indeed, this morning’s October payrolls report showed that hiring bounced back from the previous month’s hurricane-related disruptions (Chart 1). Additionally, the ISM manufacturing index components including new orders, production, and employment have held near cycle highs since mid-year and indicate that the sector is on solid footing, supported by strong domestic and foreign demand.

Volatility as a result of Hurricanes Harvey and Irma skewed data released this week, but the outlook for the fourth quarter remains positive and is helped by a solid finish to the third quarter. Strength in consumer spending in September, notably on durable goods, sets the stage for another strong showing from households in the fourthquarter. This was echoed in October’s vehicle sales which remained elevated as consumers replaced flooded cars, something that is expected to gradually fade in the months ahead. A tighter labor market should act to support household spending further. Indeed, this morning’s October payrolls report showed that hiring bounced back from the previous month’s hurricane-related disruptions (Chart 1). Additionally, the ISM manufacturing index components including new orders, production, and employment have held near cycle highs since mid-year and indicate that the sector is on solid footing, supported by strong domestic and foreign demand.

While real activity remains rosy, inflation continues to disappoint. Core PCE held steady in September at 1.3% y/y (Chart 2), while wage growth disappointed in October, rising only 2.4% y/y. Weak inflation continues to confound the FOMC, leading the committee to leave its policy rate unchanged this week. However, as the unemployment rate continues to push further below its natural rate, inflation is likely to gain traction in the year ahead and is expected to reach its 2.0% target late in 2018. We expect that these pressures should give the Fed enough ammunition to proceed with a rate hike this December.

Katherine Judge, Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.