FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- After last week’s ‘Goldilocks’ jobs report, the positive data stream continued for the U.S. economy, with retail spending in September rising by the most in three months.

- Taken together, both reports provide confirmation that the American consumer will remain a key driver of economic growth as we slowly approach the very important holiday shopping season.

- The data appear to be falling in line with expectations of most Fed officials telegraphed in the minutes of the September FOMC meeting.

- Though a rate hike a week before the November election remains unlikely, the Fed looks increasingly likely to slip in an increase before year-end so long as data continues to cooperate and downside risks do not materialize.

[su_row][su_column size=”1/2″]

[/su_column]

[su_column size=”1/2″]

[/su_column][/su_row]

FOMC MINUTES FRONT AND CENTER ALONG WITH RETAIL SALES REPORT

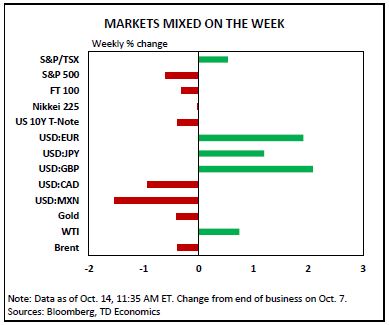

The minutes from the September 20-21st FOMC meeting and speeches from a few Fed officials, along with the September retail sales report took center stage on the domestic calendar this week. The international calendar was relatively light, with few notable data out of China dominating headlines. Overall, the Chinese data disappointed, while domestic releases were far more  constructive and communication from the Fed continued to point to a slightly hawkish tilt. Indeed, U.S. treasuries sold-off across the curve with the 10-year gaining nearly 5 bps on Tuesday alone, to end the week higher at 1.77%, at the time of writing. According to the September meeting minutes, participants generally agreed that the case for a rate hike has strengthened. Several members of the Committee stated that the decision to wait was a close call, with some indicating that a hike could come “relatively soon.” These opinions were corroborated by several Fed members, with many suggesting that a December hike remains appropriate, with Chair Yellen’s highly anticipated speech this afternoon likely to further shed light on the Fed thinking.

constructive and communication from the Fed continued to point to a slightly hawkish tilt. Indeed, U.S. treasuries sold-off across the curve with the 10-year gaining nearly 5 bps on Tuesday alone, to end the week higher at 1.77%, at the time of writing. According to the September meeting minutes, participants generally agreed that the case for a rate hike has strengthened. Several members of the Committee stated that the decision to wait was a close call, with some indicating that a hike could come “relatively soon.” These opinions were corroborated by several Fed members, with many suggesting that a December hike remains appropriate, with Chair Yellen’s highly anticipated speech this afternoon likely to further shed light on the Fed thinking.

The key point of contention in the discussion had to do with the amount of remaining slack in the labor market. Some believed that slower payroll growth and a pickup in wages recently indicated “little or no remaining slack.” Others viewed wage growth as still-muted and argued that rebounding labor force participation suggested that slack remained. Markets reacted by upping the probability of a December hike above two-thirds, from closer to 60% the previous week. The USD also saw broad-based strength throughout the week, with the DXY rising by 1.3% through this morning.

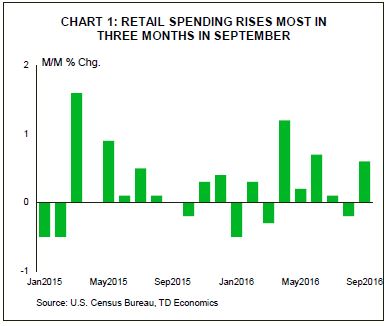

Following the minutes, markets turned to this morning’s retail sales report. After two months of relatively subdued performance, retail sales rose 0.6% in September (Chart 1). Figures for the two prior months were also revised up slightly. Overall, the bounce back in September fell in line with last week’s ‘Goldilocks’ employment report (Chart 2) and taken together, these provide confirmation that the American consumer should remain a key driver of economic growth.

On the other hand, international data was less constructive. Trade data out of China for September painted a rather grim picture. The trade surplus narrowed from $52.05bn to $USD42.0bn as exports fell sharply during the month, raising concerns of a sharper slowdown. Concerns around a ‘hard-Brexit’ also continued to surface, sending the British pound another 2.0% lower vis-à-vis the USD over the past week. Despite the Fed viewing near-term risks as “roughly balanced” at this point, both of these developments highlight the need for these developments to be closely monitored. – something the Fed intends to do.

While a softer global economy remains the current reality, domestically the data continues to come in relatively constructively. As long as this progress is maintained, a data-dependent Federal Reserve will likely remain on track to raise interest rates in the near future. Although a rate hike a week before the November election remains unlikely, the Fed appears increasingly likely to slip in an increase before year-end.

Neil Shankar, Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.