FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- U.S. equities this week managed to recover from earlier losses following strong earnings and a series of upbeat economic

data. Durable goods orders and new home sales surprised to the upside, while the House approved a budget

plan, adding to the upbeat tone. - The advance estimate for third quarter GDP growth of 3% (annualized) came in better than expected despite hurricane

impacts weighing on domestic demand. - The ECB announced a reduction in its pace of asset purchases and extended its bond-buying program through September

2018 or beyond if necessary, acting to affirm a growing policy divergence between the ECB and the Fed.

U.S. Economy Steams Ahead at 3% Pace

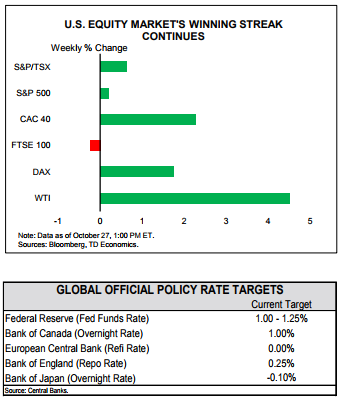

Financial Stocks gained this week on the back of strong earnings reports and on upbeat economic data. Durable goods orders rose 2.2% (m/m) in September – more than double the expected rate, while new home sales surged an impressive 18.9%. Although the latter can be partially attributed to a rebound in hurricane-hit areas, improvements were recorded in all regions, as activity was likely boosted by significant inventory shortages in the existing home market. The passing of a budget plan in the House, another step forward toward tax reform, added to the upbeat tone and proved particularly beneficial to Treasury yields and the U.S. dollar.

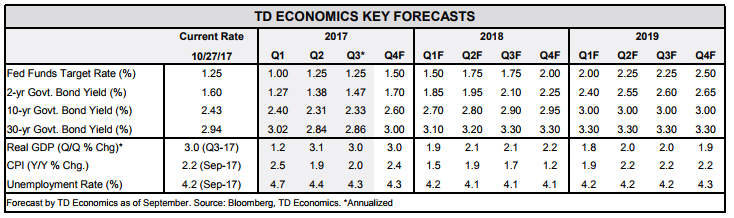

The most anticipated report of the week, BEA’s advance GDP estimate, reflected this positive momentum. Growth for the third quarter came in much better than anticipated, with the economy expanding at 3% (Q/Q annualized) despite hurricane impacts. The latter did appear to weigh on a few categories, such as services spending and both residential and non-residential construction, all of which dragged on domestic demand (Chart 1), although inventory restocking helped provide some offset. Net trade also contributed positively to growth, but likely reflected a hurricane-related fall in imports, suggesting some giveback ahead. Still, with rebuilding likely to lift fourth-quarter economic growth via a rebound in domestic demand, another print of around 3% appears to be in the cards. Given estimated trend growth of 2.0%, another quarter of above trend growth is consistent with a continuation of the current interest rate hiking cycle. As such, a December rate hike appears very likely, provided that we also see some cooperation from inflation metrics.

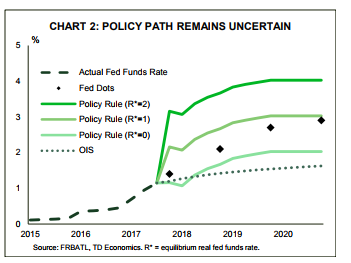

Beyond 2017 however, the interest rate path is more uncertain. This is not only due to evolving growth and inflation dynamics, but also a possible radical makeover of the Fed, which has a number of open Board of Governor positions and may soon get a new Chair. Among the frontrunners for the top position, former Fed Governor Kevin Warsh and Stanford professor John Taylor are regarded as somewhat of a challenge to the status quo, given their apparent preference for a more rules-based approach to setting interest rates. The current Fed under Chair Yellen views monetary policy rules more as guideposts and argues against a mechanical approach, the shortcomings of which include the failure to capture current cycle dynamics

and the difficulty in measuring the input variables. The latter can lead to significantly different paths (Chart 2, see report). Nevertheless, in the event that a strict rules based approach to monetary policy is implemented, it would point to a faster pace of interest rate normalization.

A number of humdrum central bank meetings took place thisweek,with Canada, Sweden and Norway keeping rates on hold. In contrast, the ECB meeting was more eventful as it announced an open-ended extension of its asset purchase program through September 2018 and a reduction in its pace of asset purchases to €30B/month starting in January 2018 from the present €60B pace. However, monetary policy is likely to remain loose in the Euro Area for some time as it lags the U.S. on both the inflation and employment front. This divergence in monetary policy is likely to remain a key driver of exchange rate moves for the foreseeable future.

Admir Kolaj, Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.