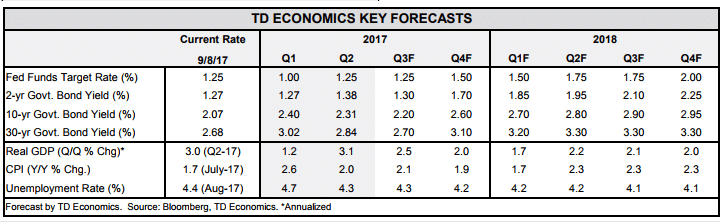

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Investors had lots to digest this week, with the lineup including communication from central banks, natural disasters and growing geopolitical tensions. The dynamics weighed on equities, while sending gold and Treasuries higher. Economic data remained largely positive, but diverging views among Fed officials point to some uncertainty as to the near-term path of interest rates. The October departure of Vice Chair Fischer is likely to add to that uncertainty.

- Economic data is likely to sustain some volatility due to the effects of Hurricane Harvey and the impending Hurricane Irma. Today’s swift deal in Congress to extend the government’s funding and borrowing limit until Dec. 8th, along with a $15.25 bn. relief package, should nonetheless provide some solace for the economy.

[su_row][su_column size=”1/2″]

[/su_column]

[su_column size=”1/2″]

[/su_column][/su_row]

More Stormy Weather And Volatile Data On The Horizon

Despite this being a holiday-shortened week, investors had lots to digest, with the lineup including communication from central banks, natural disasters and growing geopolitical tensions. The latter was the dominating factor at the start of the week, with markets opening on a dour note as investors poured into safe haven assets. The dynamic sent gold and Treasuries higher, while also benefitting crude oil. Conversely, long-term yields and the trade-weighted U.S. dollar sustained their downward trends – the latter falling to early 2015 levels.

Nonetheless, the theme of synchronized economic growth leading to a removal of monetary stimulus was back on display this week. An improved performance of the Eurozone and Canadian economies, which have been growing at rates significantly above potential lately, inspired more hawkish stances among their central banks. In this vein, the BoC hiked its key interest rate for the  second time in two months, while the ECB began having ‘very preliminary discussions’ about how to scale back its €60 bn/month asset purchase program, with the process likely to start next year.

second time in two months, while the ECB began having ‘very preliminary discussions’ about how to scale back its €60 bn/month asset purchase program, with the process likely to start next year.

U.S. economic data was similarly positive. The trade deficit remained largely unchanged in July, and net exports are on track to contribute positively to economic activity for the third consecutive quarter. At the same time, the ISM non-manufacturing index followed its manufacturing counterpart and rebounded in August. The renewed vigor in both ISM metrics points to economic growth gaining momentum, with an upbeat tone in the Beige Book echoing a similar narrative. What is more, the prices paid components of both indices continued to point Admir Kolaj, Economist to rising price pressures (Chart 1). While we are yet to see these manifest in inflation metrics, the trend should still provide some comfort to the Fed as it meets to discuss monetary policy in two weeks’ time.

Ahead of that meeting, a number of speeches from Fed officials took place throughout the week. The most significant were those of voting members Brainard and Dudley. Brainard’s speech, which suggested treading carefully over low inflation, was decisively dovish. Meanwhile, Dudley retained a more hawkish tone, but did acknowledge his ‘surprise’ to the shortfall in inflation and suggested that ‘structural’ factors may be at play. The diverging views point to some uncertainty as to the nearterm path of interest rates. The October departure of Vice Chair Fischer, at a time when the Fed Board already has three vacancies, is likely to add to that uncertainty.

This comes at a time when economic data is bound to go through some volatility due to the effects of Hurricane Harvey and the impending Hurricane Irma. Case in point, the weak August auto sales report has already been followed by a spike in jobless claims this week (Chart 2). The theme also played out in the Beige Book which, despite its upbeat tone, highlighted Harvey-related disruptions ahead. We expect these transitory effects to leave economic growth largely unchanged over the medium-term, but they will likely weigh on near-term economic activity (see commentary). Today’s swift deal in Congress to extend the government’s funding and borrowing limit until Dec. 8th, along with a $15.25 bn. relief package, should nonetheless provide some solace.

This comes at a time when economic data is bound to go through some volatility due to the effects of Hurricane Harvey and the impending Hurricane Irma. Case in point, the weak August auto sales report has already been followed by a spike in jobless claims this week (Chart 2). The theme also played out in the Beige Book which, despite its upbeat tone, highlighted Harvey-related disruptions ahead. We expect these transitory effects to leave economic growth largely unchanged over the medium-term, but they will likely weigh on near-term economic activity (see commentary). Today’s swift deal in Congress to extend the government’s funding and borrowing limit until Dec. 8th, along with a $15.25 bn. relief package, should nonetheless provide some solace.

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.