HIGHLIGHTS OF THE WEEK

- Fears of fresh elections in Italy spooked investors, who unloaded Italian bonds – sending yields on short-term government debt skyrocketing. By the end of the week, Italy’s populist coalition was finally allowed to form a government. But far from closure, this likely marks the beginning of a new chapter that will test the Eurozone’s stability.

- The U.S. turned up the heat on trade tensions by announcing that it would go ahead with tariffs on $50B of Chinese goods, and that it would end the exemption on steel and aluminum tariffs for Canada, Mexico and the EU.

- By the end of the week, markets shrugged off the latest developments in Europe and on trade, supported by a string of positive U.S. data – in particular, a very healthy May payrolls gain of 223k and wage growth that accelerated to 2.7% y/y. The latest data cement the case for a Fed rate hike at its June meeting.

Nessun Dorma (No One Sleeps)

The theatrical twists and turns of this week’s events are worthy on an opera, with the opening act set in Italy. Political turmoil and fears that new elections in Europe’s fourth largest economy could strengthen the grip of Eurosceptic parties spooked investors, who began to unload Italian assets. This sent yields on short-term government debt skyrocketing (Chart 1). Investors also steered clear of other southern European debt, with short-term Spanish, Greek and Portuguese bonds also selling off. Concerns regarding new elections subsided as the week wore on, and these moves began to reverse course. By the end of the week the populist coalition was allowed to form a government. Still, the fact that the new Italian government – which favors tax cuts and spending  increases – is likely to clash with the E.U. on a number of issues, suggests that this is merely a new chapter which may further tests the bloc’s stability. The sheer size of Italy’s economy – roughly ten times that of Greece – will warrant special attention.

increases – is likely to clash with the E.U. on a number of issues, suggests that this is merely a new chapter which may further tests the bloc’s stability. The sheer size of Italy’s economy – roughly ten times that of Greece – will warrant special attention.

Markets were thrown another curve ball when the White House announced that it would be pushing ahead with tariffs on $50B of Chinese goods and end the exemption on steel and aluminum tariffs for the E.U., Canada and Mexico. These normally close allies pledged to challenge the tariffs through the WTO and NAFTA channels and levy retaliatory tariffs. At around $12.6B and $7.7B of U.S. products targeted by Canada and the E.U. respectively, and an estimated $4B in trade with Mexico, the amount of affected trade is still quite small. But the wide list of products marked for tariffs, which stretch from agricultural products to motorcycles, are sure to strike a sour cord with the U.S. Ultimately, the tariffs will make goods more expensive for the American consumer. In a prior analysis, in which we expected the exemptions for the allies to stay, we estimated that the tariffs would have a muted direct impact on U.S. economic activity and inflation. The recent events make us more confident that while the impact on U.S. economic activity is still expected to be limited, the tariffs are likely to boost consumer price inflation by at least 0.1 percentage points this year and next.

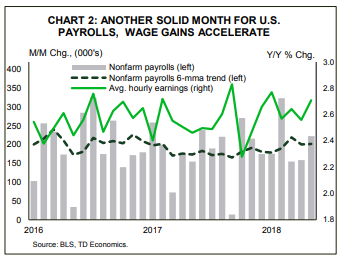

Behind the curtain of the unfolding Italian and trade sagas, U.S. economic data was broadly positive. American consumers were back in full force in April, with personal spending rising by a robust 0.4% in real terms, building on a solid March print. The back-to-back gains point to a 3.5% rebound in second quarter consumer spending after a soft first-quarter print (1% Q/Q ann.). This narrative is further reinforced by a strong labor market. In May, payrolls gains (223k) beat expectations, the unemployment rate fell to an 18-year low (3.8%) and wage growth accelerated to 2.7% y/y (Chart 2). Rounding out the good economic news was an above-consensus print in the ISM manufacturing index, which pointed to manufacturing activity accelerating in May.

Behind the curtain of the unfolding Italian and trade sagas, U.S. economic data was broadly positive. American consumers were back in full force in April, with personal spending rising by a robust 0.4% in real terms, building on a solid March print. The back-to-back gains point to a 3.5% rebound in second quarter consumer spending after a soft first-quarter print (1% Q/Q ann.). This narrative is further reinforced by a strong labor market. In May, payrolls gains (223k) beat expectations, the unemployment rate fell to an 18-year low (3.8%) and wage growth accelerated to 2.7% y/y (Chart 2). Rounding out the good economic news was an above-consensus print in the ISM manufacturing index, which pointed to manufacturing activity accelerating in May.

The latest data cement the case for a Fed rate hike on June 13th. But this is no time to fall asleep, with further policy rate normalization also requiring a watchful eye on developments out of Europe and the potential fallout from heightened trade tensions. For now, Nessun Dorma.

Admir Kolaj, Economist | 416-944-6318

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.