HIGHLIGHTS OF THE WEEK

- Investor optimism recovered following the softening of China’s stance to the recent U.S. tariffs while the renegotiated KORUS trade deal with South Korea also bodes well for stateside producers.

- February’s consumer spending report indicated progress on the inflation front. However, weak consumer spending will weigh on GDP growth in the first quarter which is expected to advance by less than 2%.

- Consumer strength should reassert itself as the year progresses alongside a tightening labor market and tax cuts, enabling the Fed to raise rates two more times this year.

Soft Spending Suggests Another Weak Q1

It was a relatively quiet week for economic data with investors turning their attention to political developments. Investor optimism recovered following the softening of China’s stance to the recent U.S. tariffs. The Middle Kingdom appeared to be backing down from retaliatory tariffs previously threatening U.S. cars, wine, and food products, instead appearing increasingly open to improving U.S. access to Chinese markets. This should benefit several regional economies that rely on exports to China. As we noted in our recent State Economic Forecast, over one third of South Carolina’s auto exports are destined for China, and their share is rising. Furthermore, the renegotiated KORUS trade deal with South Korea doubles the number of vehicles allowed to be exported from American carmakers and contains a commitment from South Korea to reduce steel exports to the U.S. by 30%, adding to the positive prospects for domestic producers. The constructive trade developments led the greenback higher over the week, but gains in major equity indices were restrained by tech sector induced volatility.

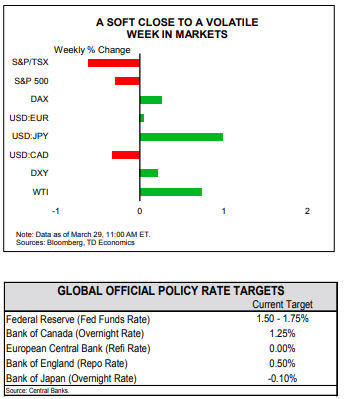

It was a relatively quiet week for economic data with investors turning their attention to political developments. Investor optimism recovered following the softening of China’s stance to the recent U.S. tariffs. The Middle Kingdom appeared to be backing down from retaliatory tariffs previously threatening U.S. cars, wine, and food products, instead appearing increasingly open to improving U.S. access to Chinese markets. This should benefit several regional economies that rely on exports to China. As we noted in our recent State Economic Forecast, over one third of South Carolina’s auto exports are destined for China, and their share is rising. Furthermore, the renegotiated KORUS trade deal with South Korea doubles the number of vehicles allowed to be exported from American carmakers and contains a commitment from South Korea to reduce steel exports to the U.S. by 30%, adding to the positive prospects for domestic producers. The constructive trade developments led the greenback higher over the week, but gains in major equity indices were restrained by tech sector induced volatility.

Global equity markets fared better as trade tensions thawed. However, trade uncertainty still lingers in Europe, with only four weeks until a temporary exemption from U.S. imposed steel and aluminum tariffs expires. The EU is contemplating lowering tariffs on a range of U.S. goods including cars, machinery, pharmaceuticals, and food in hopes of averting a trade war. However, the “carrot” approach is not favored by all members of the EU, including France. That could result in higher volatility in global equity markets in the weeks ahead.

Long-term yields fell this week in the U.S., while yields on two-year Treasury notes rose. Short-term yields are poised to rise further over the medium-term as the Federal Reserve continues along its tightening path amidst higher government spending. President Trump’s $1.3 trillion spending bill, signed last Friday, adds to the early-February commitment of $288 billion in domestic and military spending over the next two years which will amplify fiscal pressures. These will lead to higher Treasury issuance and should lift bond yields that will be further supported by rising inflation expectations and interest rates as the global economic recovery continues.

Long-term yields fell this week in the U.S., while yields on two-year Treasury notes rose. Short-term yields are poised to rise further over the medium-term as the Federal Reserve continues along its tightening path amidst higher government spending. President Trump’s $1.3 trillion spending bill, signed last Friday, adds to the early-February commitment of $288 billion in domestic and military spending over the next two years which will amplify fiscal pressures. These will lead to higher Treasury issuance and should lift bond yields that will be further supported by rising inflation expectations and interest rates as the global economic recovery continues.

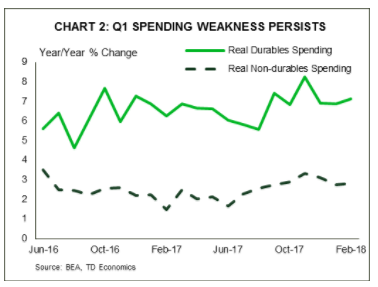

February’s consumer spending report indicated progress on the inflation front. Core PCE inflation ticked up slightly (Chart 1), with price gains over the recent three months averaging 2.3% in annualized terms. We expect this strength in inflation to continue, supported by diminishing slack in the U.S. economy, rising global economic activity, a relatively weak USD, and the fading of idiosyncratic factors. However, other details of the report were less encouraging. Consumer spending came in soft (Chart 2), adding to January’s disappointment, and weighing on GDP growth in the first quarter, which is still expected to advance by less than 2%. Still, we believe that consumer strength will reassert itself as the year progresses alongside a tightening labor market and tax cuts. Such a backdrop should enable the Fed to continue gradually raising interest rates this year, with another two hikes expected this year before 75 basis points of increases during 2019.

Katherine Judge, Economist | 416-307-9484

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.