FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Stocks are poised to finish the week in positive territory for the first time in a month, helped by a good start to earnings season which suggests the U.S. profit recession is likely coming to an end.

- U.S. data remains supportive of a near-term rate hike with wage pressures broadening. Speeches by Fischer and Dudley this week suggest both are in favor of a rate hike this year given the current trajectory.

- The Chinese economy expanded 6.7% from a year ago in Q3, helping assuage fears that it is slowing more abruptly than anticipated. Consumption and fixed investment supported growth while industrial production disappointed. Despite the solid print, concerns about unsustainable credit growth remain.

- The ECB left policy rates and QE program framework unchanged this week, punting any policy refresh to December. ECB President Draghi adamantly talked down any notions of near-term tapering of asset purchases, emphasizing that policy will remain accommodative even after any eventual reduction in QE.

[su_row][su_column size=”1/2″]

[/su_column]

[su_column size=”1/2″]

[/su_column][/su_row]

WAITING FOR DECEMBER

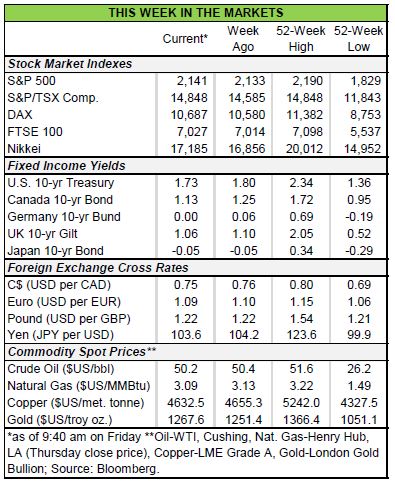

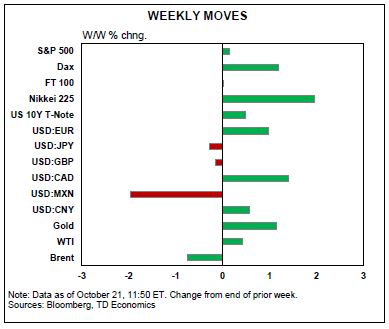

Sentiment was good in global markets this week. Stocks look to finish the week in positive territory for the first time in a month. Earnings season was off to a good start in the U.S. with the U.S. profit recession likely to come to an end. U.S. longer term bond yields remained rangebound, while shorter dated securities continued to sell-off in anticipation of a near-term Fed hike. The dollar benefitted, rising to its highest level since February, on relatively constructive data and hawkish Fedspeak. Investor sentiment was also shored up by the ECB and positive Chinese data.

The world’s second largest economy expanded 6.7% from a year ago in Q3, helping assuage fears that it is slowing more abruptly than anticipated. On the whole, industrial production disappointed, but activity was shored up by fixed investment and consumption. While concerns that growth remains tied to unsustainable credit expansion remain, investors were nonetheless comforted by the figures with sentiment further supported by the reappearance of inflation. Nominal GDP advanced by 7.8% y/y in the quarter, with the GDP deflator advancing by the fastest pace in two years as drag from past commodity declines dissipates.

Inflation is also improving in the Eurozone, with headline prices up 0.4% in September and core CPI up an even stronger 0.5%. Still, the ECB’s Governing Council remains unconvinced that underlying inflationary pressures are building. The ECB left policy rates and QE program framework unchanged this week, as widely expected, with President Draghi punting any policy refresh to December – a meeting that will correspond with updated economic forecasts. Importantly, Draghi adamantly talked down any notions of near-term tapering of asset purchases, which caused a

sell-off in Eurozone bond markets, further emphasizing that policy will remain accommodative even after any eventual reduction in asset purchases.

Monetary policy will also remain highly accommodative in the U.S. despite the likely quarter-point increase in the fed funds rate target later this year. Chair Yellen’s speech last week, where she  highlighted the potential benefits of a “high-pressure” economy, had a somewhat dovish-tilt, but Vice-Chair Fischer on Monday instead emphasized that the economy was “very close to [the Fed’s] targets,” auguring for a near-term hike. The sentiment was corroborated by New York President Dudley, who is a permanent FOMC voting member, and believes the Fed is “reasonably close” to its targets with a rate hike “appropriate” if the economy remains on its current trajectory.

highlighted the potential benefits of a “high-pressure” economy, had a somewhat dovish-tilt, but Vice-Chair Fischer on Monday instead emphasized that the economy was “very close to [the Fed’s] targets,” auguring for a near-term hike. The sentiment was corroborated by New York President Dudley, who is a permanent FOMC voting member, and believes the Fed is “reasonably close” to its targets with a rate hike “appropriate” if the economy remains on its current trajectory.

Data released this week remained supportive of such narrative. While housing starts and initial claims disappointed somewhat, these may have been distorted by Hurricane Matthew. On the other hand, building permits and existing home sales both surprised to the upside, suggesting continued housing recovery. Inflation was also relatively firm, with headline CPI accelerating to 1.5% while the core measure remained just above 2% in September. Lastly, the recent Beige Book highlighted broadening labor shortages and wage pressures, corroborated by the 3.6% y/y gain in median wages. On the whole, both reports reinforce the notion that inflationary pressures in the U.S. are building and provide additional impetus for a rate hike in December.

Michael Dolega, Senior Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.